The short answer: borrow carefully, and only after you know the real project range

Many homeowners focus on the monthly payment first. That is where people get trapped.

A pool is usually a want, not an emergency repair. If you borrow, ask one question before anything else: Can I still afford this if the project ends up 15% to 25% higher than my first estimate? If the answer is no, pause.

Typical in-ground pool build ranges are often around $60,000 to $135,000 for gunite/concrete, $45,000 to $95,000 for fiberglass, and $35,000 to $70,000 for vinyl-liner. Smaller or plunge-style pools can cost less. But the real price depends on pool type, size, access to the yard, soil, slope, finishes, equipment, and your area. You can review more detail on pool costs and compare options in this pool type comparison guide.

Borrowing may make sense if:

- your emergency savings stay intact after the deposit and early payments

- the payment fits your monthly budget without counting on overtime, bonuses, or future raises

- you have room for changes like fencing, drainage, electrical upgrades, or permit costs

- you are hiring licensed, insured, and bonded builders, and you verify that yourself

Borrowing is risky if:

- you only know the base pool price, not the full outdoor project price

- the lender is pushing speed over clarity

- the builder contract is vague on scope, allowances, change orders, and payment timing

- you would need to skip safety items, fencing, or needed site work to make the payment work

DeepEnd Match is a free matching service. We do not build pools or give financial, legal, tax, or lending advice. We help you get matched with builders so you can compare written price and scope, ask better questions, and choose who to hire. If you want to start there, use Get Matched.

Questions to ask yourself before you ask a lender

Before you compare loan offers, get honest with yourself about the project.

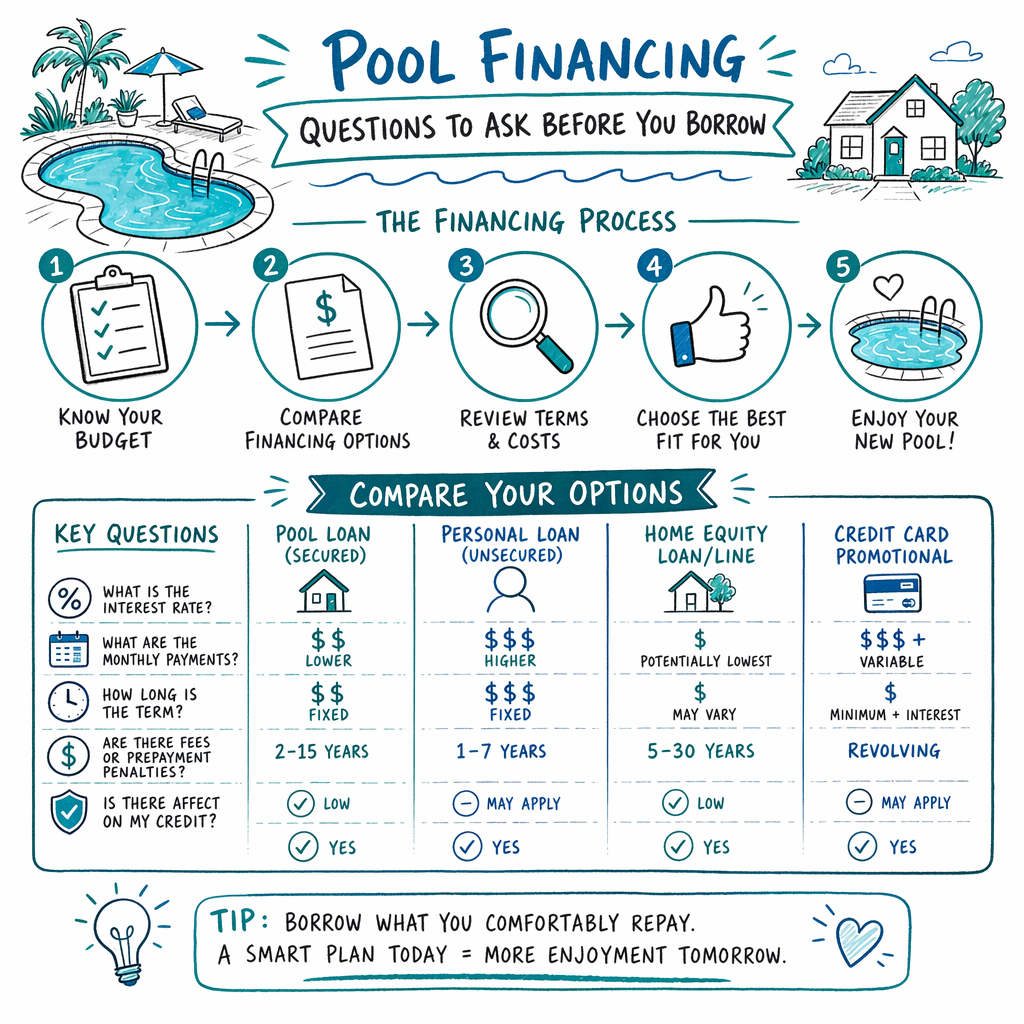

1. What is my full budget, not just the shell?

Pool buyers often forget decking, fencing, alarms, landscaping repairs, drainage, retaining walls, extra concrete, patio covers, heaters, automation, and higher electric bills.

2. What problem am I solving?

Is this for family use, exercise, hot weather, or resale appeal? If your reason is weak, debt will feel heavier later.

3. How long do I plan to stay in this home?

A pool may add enjoyment, but it does not always return full cost at resale.

4. Can I handle pool ownership after construction?

Cleaning, chemicals, water, repairs, insurance changes, and seasonal opening or closing all cost money.

5. Do I have cash for surprises?

Even with a good plan, site conditions can change. A rocky dig, poor access, drainage issues, or utility conflicts can add cost.

A simple rule many homeowners use: keep a separate contingency fund beyond the expected build amount. The exact amount is your choice, but having one matters.

Also ask the builder these practical questions before you borrow based on any number:

- What exactly is included in the written scope?

- What is listed as an allowance instead of a fixed included item?

- What common upgrades change the price later?

- What site conditions can increase cost?

- What permits, inspections, and safety-barrier items are required locally?

Read our guides on how to vet a pool builder and pool permits explained before you sign anything.

Questions to ask the lender before you sign

You do not need to be a finance expert to protect yourself. You just need to ask direct questions and insist on clear answers in writing.

Use this checklist:

- What is the interest rate, and is it fixed or variable?

A low starting rate can rise later if it is variable.

- What is the APR?

APR can give a better picture of total borrowing cost because it may include certain fees.

- What are the fees?

Ask about origination fees, closing costs, annual fees, late fees, and prepayment penalties.

- What is the loan term?

A longer term can lower the monthly payment but raise the total amount paid over time.

- What is the monthly payment at today’s terms, and what is the total paid over the full term?

Look at both numbers, not just the monthly amount.

- When does repayment start?

Some homeowners are surprised that payment starts before the pool is finished.

- How are funds released?

Is money paid in stages? Who approves each draw? What happens if there is a dispute?

- Can rates or terms change if the project cost changes?

If your project goes over budget, will you need a second loan or cash?

- What happens if construction is delayed?

Weather, permit delays, and inspections can affect timing.

- Is there any penalty for paying off early?

That matters if you may refinance or pay down the loan faster.

Then ask yourself one more hard question: If this pool ends up costing more and taking longer, do I still want it?

Do not let anyone rush you because a promotion is ending or a slot is filling. A clear written loan offer beats a fast verbal promise every time.

How homeowners get burned, and how to avoid it

Most expensive mistakes happen before the first dig.

Here are common trouble spots:

- Borrowing from a guess

A homeowner hears a base price like "$50,000" and borrows near that amount. Later, access issues, upgraded equipment, decking, and fencing push the real project much higher.

- Comparing payments, not total cost

A lower monthly payment over many years can cost far more overall.

- Signing vague contracts

If the scope is loose, change orders can pile up. Get the price, scope, materials, equipment, finish details, schedule, and payment stages in writing before any deposit.

- Skipping license and insurance checks

Always hire licensed, insured, and bonded builders where required, and verify the license, insurance, and bond yourself. Do not rely only on a logo, ad, or verbal claim.

- Paying too much too soon

Do not hand over large money without a written contract and a clear payment schedule tied to real progress.

- Ignoring safety-law costs

Fences, gates, alarms, covers, and inspections may be required. Review local rules and see this guide on pool safety barriers.

A simple protective approach:

- Get at least two detailed written proposals.

- Compare the same scope, not just the headline price.

- Verify license, insurance, and bond yourself.

- Confirm permit responsibility and safety-barrier requirements.

- Keep control of the final payment until the agreed work is complete under the contract terms.

You compare quotes. You choose who to hire. You hold the final payment.

What to do next before you borrow

If you are serious about building, do these steps in order:

1. Choose the pool type that fits your budget and yard.

Gunite, fiberglass, and vinyl-liner pools have different price ranges, timelines, and long-term upkeep. See the service pages for gunite/concrete pools, fiberglass pools, or vinyl-liner pools if you want a starting point.

2. Build a real all-in budget.

Include the pool, deck, fencing, permits, electrical, drainage, cleanup, and a cushion for surprises.

3. Get matched with builders and collect written scopes.

DeepEnd Match is free for homeowners. Participating builders pay a flat fee to participate. You can start at Get Matched.

4. Compare financing only after you have realistic project numbers.

Do not finance from a rough guess or a marketing teaser price.

5. Read every contract line before any deposit.

Make sure price, scope, materials, equipment, timeline, change-order terms, and payment stages are written clearly.

Remember: no lender, salesperson, or builder should make you feel embarrassed for asking basic money questions. This is a major home project. Slow is normal. Careful is smart.

Do not borrow for a pool until you know the real all-in project range, not just the base pool price. Get detailed written proposals, verify the builder’s license, insurance, and bond yourself, compare loan terms carefully, and make sure the payment still works if the project costs more than expected.

Common questions

Is it a bad idea to finance a pool?

Not always. It depends on your budget, savings, and how stable your income is. The main risk is borrowing based on a low initial estimate and then getting hit with extra project costs. Before you sign, make sure the full project still works if the final price is higher than the first number you heard.

What costs do homeowners forget when planning pool financing?

Common misses include decking, fencing, alarms or other safety items, permits, electrical work, drainage, landscaping repair, retaining walls, heaters, automation, and ongoing maintenance. The real cost depends on the pool type, size, site, finishes, and your area.

Should I get financing before talking to pool builders?

Usually, start by understanding realistic project ranges and getting written scopes from licensed, insured, and bonded builders. That gives you better numbers to use when comparing loans. If you shop loans first, you may anchor to the wrong budget.

What should I verify before paying a deposit?

Verify the builder’s license, insurance, and bond yourself. Get the full price and scope in writing, including materials, equipment, payment stages, and change-order terms. Confirm who handles permits and make sure the project follows local permit and pool-safety or fencing laws. Keep control of the final payment until the agreed work is complete under the contract terms.