Start with the real pool price, not the monthly payment

Many people shop by monthly payment first. That is where people get trapped. A low monthly number can hide a higher total cost over time.

For a typical in-ground pool, many homeowners see rough starting ranges like:

- Gunite/concrete: about $60,000-$135,000

- Fiberglass: about $45,000-$95,000

- Vinyl-liner: about $35,000-$70,000

- Smaller plunge pools: often less, depending on size and site

These are typical ranges, not quotes or guarantees. The real price depends on the pool type, size, soil, access to the yard, slope, decking, drainage, water features, equipment, finishes, and your area. You can review broader ranges on our costs page.

Before you think about financing, ask each builder for the full project price and scope in writing. That should include what is included, what is excluded, what can change later, and when payments are due. You should also follow local permit and pool-safety rules. Our pool permits guide can help you understand the process at a high level.

DeepEnd Match does not make loans or give financial advice. We help you get matched, at no cost, with licensed, insured, bonded pool builders so you can compare your options yourself.

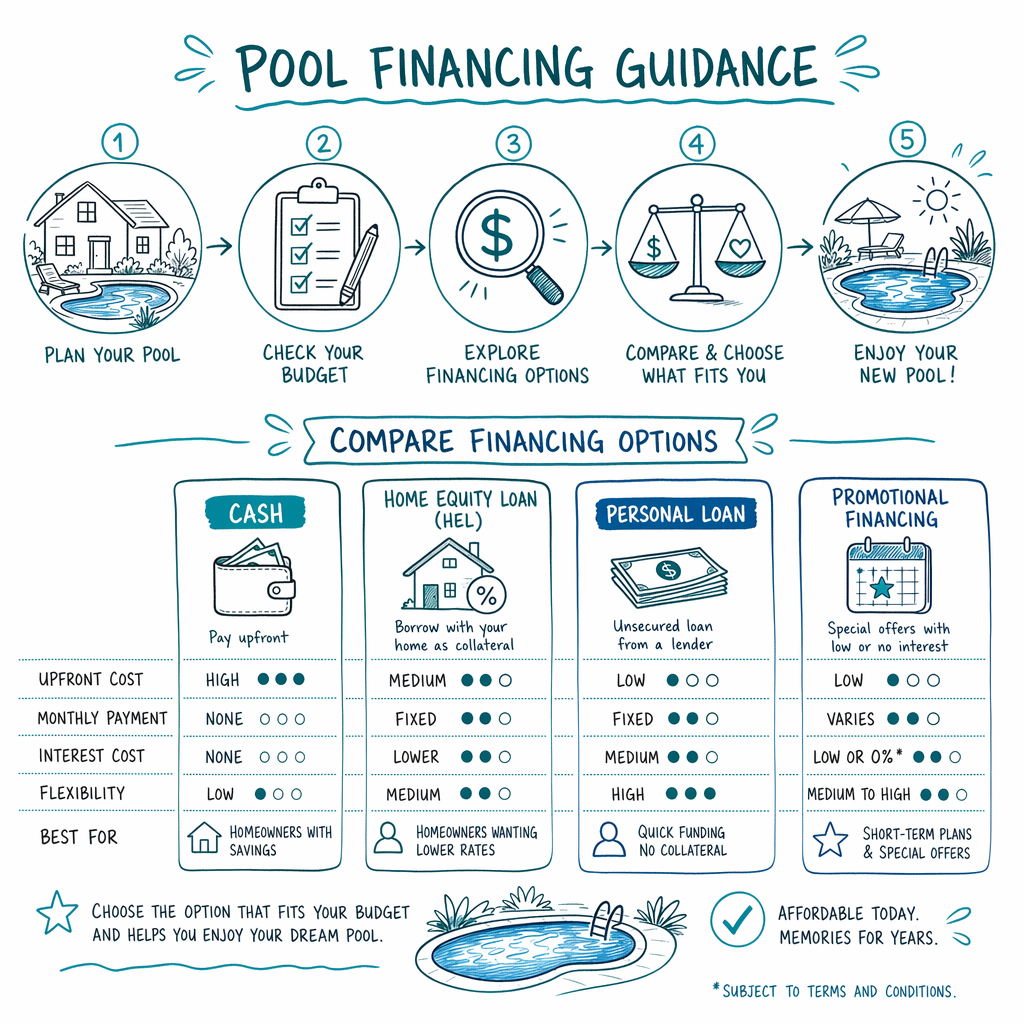

Common ways homeowners pay for a pool

There is no one best way for everyone. The right choice depends on your budget, timeline, comfort with debt, and how much risk you can handle.

1. Cash savings

- Simple and clear

- No loan payment

- Good if you still keep an emergency fund after the project

2. Home equity borrowing

- Some homeowners use home equity products for large projects

- This may offer lower rates than unsecured borrowing in some cases

- Your home may be used as collateral, so the risk is serious if payments become hard

3. Personal or unsecured loans

- Faster for some borrowers

- Usually no home collateral

- Rates can be higher, especially for longer terms or weaker credit

4. Builder-offered financing programs

- Convenient because it may be discussed during the sales process

- Easy does not always mean cheap

- Ask who the lender is, whether there are fees, and what the total paid will be over the full term

5. Phased project approach

- Some homeowners build the pool first and add extras later

- This can reduce the amount borrowed now

- Make sure the builder clearly states what is included in phase one and what future work may cost

A smart rule: compare the total project cost, the loan term, the interest rate, any fees, and the total amount repaid. Do not compare by monthly payment alone.

What changes the amount you may need to finance

The pool shell is only part of the budget. Many surprise costs happen around the pool, not inside it.

Common cost drivers include:

- Pool type: gunite/concrete, fiberglass, or vinyl liner

- Pool size, depth, and shape

- Spa, tanning ledge, waterfall, lighting, automation, heater, salt system

- Demolition, tree removal, soil problems, rock, high water table, retaining walls

- Tight yard access that needs smaller equipment or extra labor

- Decking, coping, fencing, gates, and drainage work

- Utility upgrades or equipment pad changes

- Permit fees and inspection requirements, depending on local rules

This is why two pools that look similar online can cost very different amounts in real life.

Ask every builder for a line-by-line scope. Ask them to separate:

- Base pool price

- Site work allowances

- Equipment and finish upgrades

- Permit-related items

- Fencing or safety-barrier items if not included

- Change-order pricing rules

That written detail matters because financing a project with missing scope can leave you short later. It is better to know the likely full budget up front than to borrow too little and scramble mid-project.

How the payment process usually works

The payment schedule depends on the builder and the project. But in many cases, homeowners pay in stages as work moves forward.

A typical process may look like this:

1. Planning and estimates

- You compare builders, scope, and typical price ranges

- You review what type of pool fits your budget and yard

2. Written proposal and contract

- The builder gives price, scope, payment schedule, estimated timeline, and allowance details in writing

- You review exclusions carefully

3. Deposit

- A deposit may be requested after signing

- Never rely on a verbal promise. Get the amount, refund terms, and next steps in writing before any deposit

4. Permits and scheduling

- Local approvals, engineering requirements, HOA rules, and inspections can affect timing

5. Progress payments

- Payments may be tied to milestones such as excavation, shell installation, plumbing/electrical rough-in, decking, plaster or liner, and startup

6. Final payment

- Hold final payment until the agreed work is done and you have the required documents and walkthrough

Important: you choose who to hire, you compare quotes, and you hold the final payment. Always hire licensed, insured, and bonded builders, and verify the license, insurance, and bond yourself. If you want help finding companies to compare, you can get matched for free.

Also make sure you understand local fencing and barrier rules before construction starts. Pool-safety laws vary by area, and the homeowner still needs to follow them.

Pros and cons of financing a pool

Financing is not automatically good or bad. It depends on whether the payment fits your life after the excitement wears off.

Possible pros

- You may build sooner instead of waiting years to save the full amount

- You may keep some cash available for emergencies

- You can sometimes choose a better scope now instead of doing expensive rework later

Possible cons

- Interest and fees can add a lot to the real cost

- A long term can make the monthly payment look easy while the total paid becomes much higher

- If the project runs over budget, you may need more cash than planned

- If the loan is tied to your home, the risk is bigger

A good stress test is simple:

- Can you still make the payment if insurance, taxes, childcare, or groceries go up?

- Do you have money left for startup chemicals, maintenance, repairs, and utilities?

- Are you borrowing for the pool only, or also for landscaping, fencing, furniture, and outdoor kitchen items?

If the only way the deal works is with a very long term and a very low teaser payment, slow down and review the total cost again.

Questions to ask before you sign anything

Use these questions with both lenders and builders. Short questions. Clear answers.

Questions about money

- What is the full estimated project price today?

- What could raise the price later?

- What fees are not included yet?

- What is the total paid over the life of the loan, not just the monthly payment?

- Is there a prepayment penalty?

- Are there origination or closing fees?

- What happens if permits, inspections, or weather delay the project?

Questions about the builder

- Are you licensed, insured, and bonded for this work in my area?

- Can I verify your license, insurance, and bond directly?

- Who handles permits, inspections, and scheduling, and what is my role as homeowner?

- What is the payment schedule?

- What is excluded from this price?

- How are change orders approved and priced?

- What must be finished before final payment is due?

Questions about safety and legal compliance

- What local pool-barrier and gate requirements apply here?

- What inspections are required before the pool can be used?

You can use our vet-a-builder guide when checking companies. It helps you compare scope, paperwork, and warning signs without relying on sales pressure.

How to compare builders without getting burned

The builder you hire matters as much as the financing plan. A weak contract or vague scope can ruin even a reasonable loan.

Watch for these red flags:

- Pressure to sign the same day

- A price that is far lower than everyone else without a clear reason

- Refusal to show license, insurance, or bond information

- Large deposit requests with little written scope

- Verbal promises that are not added to the contract

- No clear change-order process

- Payment schedule that is not tied to real milestones

A safer comparison process is:

- Get at least 2-3 written proposals

- Compare the same pool type, size, equipment, decking, and allowances

- Verify license, insurance, and bond yourself

- Read the schedule and exclusions line by line

- Ask who you call if there is a delay or problem

- Confirm local permits and safety-barrier requirements

If you are still deciding on pool type, review a simple pool type comparison so you are comparing the right products in the first place.

DeepEnd Match is here to make the shopping part easier. Matching is free to homeowners. Participating builders pay a flat fee to be included. We do not build pools or give quotes. We help you meet licensed, insured, bonded builders so you can compare and decide with better information.

Know the real pool price first, then compare how you would pay for it. Get 2-3 written proposals, verify each builder's license, insurance, and bond yourself, follow local permit and pool-safety laws, and do not sign or pay a deposit until price, scope, and payment terms are clear in writing.

Common questions

Can I finance the pool and the patio, fence, or landscaping together?

Sometimes homeowners try to include pool-related outdoor work in one budget, but what can be included depends on the builder, the lender, and the written project scope. The important part is to get every included item in writing and ask what is excluded. Do not assume fencing, drainage, permits, or decking are included unless the proposal clearly says so.

What monthly payment should I expect for a pool?

There is no honest one-size-fits-all number. The monthly cost depends on the amount borrowed, interest rate, fees, and loan term. A lower monthly payment can still mean a much higher total cost over time. Ask for the total amount repaid over the full term, not just the monthly number.

Should I choose the builder with financing already arranged?

Not automatically. Convenience is helpful, but you should still compare the full project price, the written scope, the payment schedule, the loan terms, and the builder's license, insurance, and bond. Easy paperwork is not the same as a better overall deal.

When should I pay the final amount?

Final payment should usually wait until the agreed work is completed according to your contract, required inspections or close-out items are handled as promised, and you have the documents and walkthrough you were told to expect. Get the payment schedule and completion terms in writing before you pay any deposit.